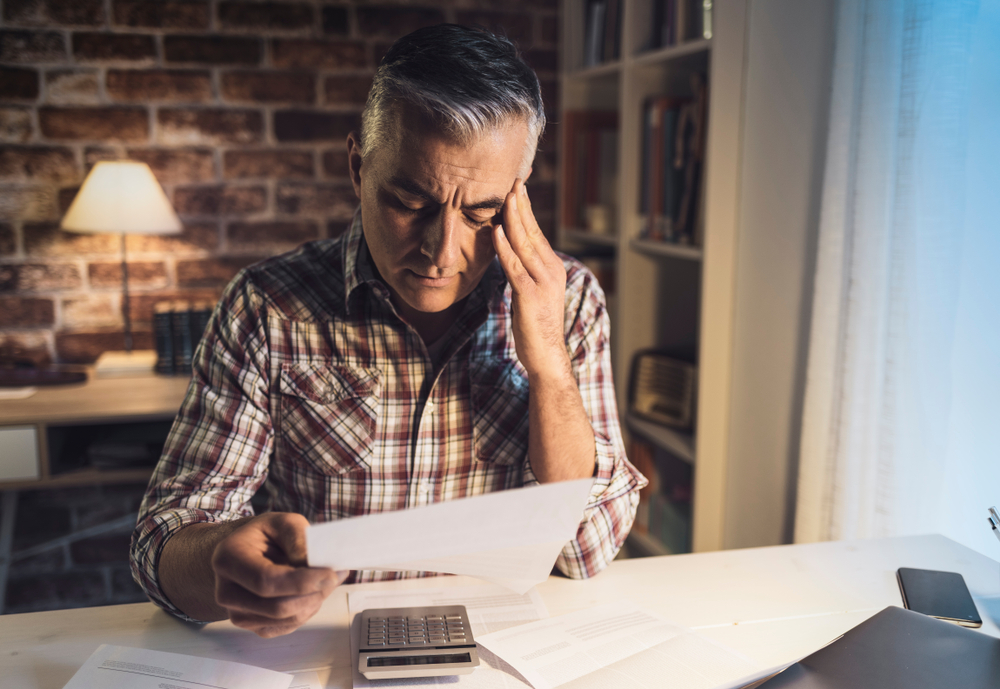

The statistics show median household income holding steady and unemployment at historic lows, creating a picture of economic health that doesn’t match what millions of Americans are experiencing daily. Financial advisors, credit counselors, and bankruptcy attorneys are reporting patterns that indicate widespread financial deterioration happening beneath the surface of official economic data—families who appeared stable a year ago now struggling with basics, middle-class households making choices between necessities, and financial buffers that took decades to build disappearing in months.

1. Credit Card Balances Hitting Record Highs

American credit card debt has surpassed $1.1 trillion, with average household balances exceeding $8,000 and rising monthly despite interest rates above 20%. The debt isn’t accumulating from luxury purchases—credit counselors report it’s groceries, utilities, and basic expenses that families can no longer cover from income alone.

The shift from using credit cards for convenience to using them for survival spending represents a fundamental change in household financial health that indicates income is no longer adequate for basic living expenses.

2. Buy Now Pay Later Usage Exploding Beyond Discretionary Purchases

BNPL services are seeing transaction volumes increase 300% year-over-year, but the purchases are no longer just for electronics and clothing—people are using payment plans for groceries, gas, and utility bills. The normalization of installment payments for consumables that should be paid from current income shows households have no cash flow buffer remaining.

When families need four installment payments to buy a week’s groceries, financial stability has already collapsed regardless of what employment and income statistics report.

3. Retirement Account Withdrawals and Loans Surging

Financial advisors report unprecedented numbers of clients taking hardship withdrawals from 401(k)s and IRAs to cover current expenses, paying taxes and penalties to access money meant for retirement. The withdrawals aren’t for emergencies like medical crises—they’re for mortgages, car payments, and basic bills that income no longer covers

The willingness to sacrifice retirement security and pay 30-40% in taxes and penalties just to cover current bills indicates financial stress severe enough to make people desperate about today regardless of tomorrow’s consequences.

4. Car Repossessions Reaching Post-2008 Highs

Auto loan delinquencies are climbing rapidly, with repossessions in 2026 approaching levels not seen since the 2008 financial crisis despite much lower unemployment. The repossessions are hitting borrowers with previously good credit who could afford payments when they bought but can’t anymore as other costs have consumed their budgets.

When people with stable employment histories are losing vehicles because monthly budgets can’t accommodate the car payment alongside inflated housing, food, and insurance costs, financial stability is clearly deteriorating across the employed middle class.

5. Healthcare Avoidance Due to Cost

Americans are skipping necessary medical care, not filling prescriptions, and avoiding preventive care at rates that alarm healthcare providers who see the decisions creating worse health problems and higher future costs. The avoidance isn’t about preferences or logistics—it’s about households that can’t afford copays, deductibles, and prescription costs even with insurance.

When families with health insurance are making medical decisions based on ability to pay rather than medical necessity, financial stability has eroded to the point where basic health maintenance becomes unaffordable.

6. Grocery Shopping Behavior Shifting Dramatically

Supermarket executives report unprecedented shifts in shopping patterns—customers buying smaller quantities more frequently as they manage cash flow day-to-day, switching from brands to generics across all categories, and increasing purchases of rice, beans, and other bulk staples that signal tight budgets.

The shopping patterns mirror behavior during recessions despite current “strong economy” narratives, suggesting household financial reality doesn’t match economic statistics. When middle-income shoppers are adopting purchasing behaviors historically associated with poverty, financial stability is clearly declining regardless of what employment numbers show.

7. Multi-Generational Housing Arrangements Increasing

Adult children moving back with parents, elderly parents moving in with adult children, and multiple families sharing housing are all increasing rapidly as standalone housing becomes unaffordable even for dual-income households. The arrangements aren’t cultural preferences—surveys show most participants would prefer independent housing but can’t afford it even with full-time employment.

The return to multi-generational housing as economic necessity rather than choice indicates that housing costs relative to incomes have made independent living financially impossible for growing numbers of Americans.

8. Side Hustle Participation Reaching Saturation

Over 45% of American workers now report having side income beyond primary employment, with the percentage continuing to climb as people discover primary jobs don’t cover expenses. The side work isn’t for extra luxuries or saving—it’s essential income that people require to cover basic bills their main jobs don’t pay enough for.

When nearly half the workforce needs multiple income streams just to maintain basic middle-class existence, financial stability has eroded to the point where standard full-time employment no longer provides adequate income for normal life.

9. Insurance Coverage Being Dropped or Reduced

Americans are dropping or reducing insurance coverage across categories—car insurance to minimum liability only, health insurance plans with catastrophically high deductibles, homeowners coverage with huge deductibles, and dental and vision coverage eliminated entirely. The coverage reductions represent calculated risks as households unable to afford comprehensive insurance choose to self-insure against disasters while freeing up hundreds monthly for immediate bills.

When households are gambling that they won’t have accidents, health crises, or house fires because they can’t afford both insurance and groceries, financial stability has deteriorated to dangerous levels that create catastrophic vulnerability.

10. Subscription Service Cancellations Accelerating

Streaming services, gym memberships, subscription boxes, and other recurring services are being cancelled at rates that alarm companies built on subscription models. The cancellations aren’t selective trimming—people are eliminating multiple subscriptions simultaneously in ways that suggest financial crisis rather than preference changes.

When households earning $75,000-$100,000 are cancelling $15 monthly streaming services, it indicates budgets are so tight that even tiny recurring expenses must be eliminated to make room for inflated costs of housing, food, and insurance.

11. Payday Loan and High-Interest Borrowing Expanding

Payday lenders, title loan companies, and other high-interest short-term lenders are reporting record business as households need bridge loans to make it to next paychecks. The borrowers increasingly include middle-income workers with decent credit who’ve exhausted conventional credit options and need cash to cover gaps between paychecks and bills.

The expansion of predatory lending into middle-class markets indicates financial buffers have disappeared and income timing mismatches that used to be minor inconveniences now require expensive short-term borrowing to prevent utilities being shut off or evictions.

12. Children’s Activities and Expenses Being Cut

Parents are pulling children from sports teams, music lessons, and other activities that require fees, equipment, or travel as these expenses become unaffordable alongside rising basic costs. The cuts represent difficult choices as parents recognize the developmental and social benefits but simply can’t afford the costs that once seemed reasonable.

When middle-class families are eliminating children’s activities that cost $50-$200 monthly, it signals household budgets are so constrained that anything beyond absolute necessities must be cut regardless of the developmental or social costs to children.

13. Emergency Fund Depletion Across Income Levels

Financial surveys show the percentage of Americans who could cover a $1,000 emergency from savings declining dramatically, with even households earning $100,000+ reporting they’d need to borrow or use credit cards for unexpected expenses. The emergency fund depletion isn’t from lack of discipline—it’s from buffers built over years being consumed by the gap between stagnant incomes and inflated costs for housing, food, healthcare, and insurance.

When households across income levels have no financial reserves remaining, the foundation of financial stability has eroded completely, leaving millions one unexpected expense away from financial crisis that spreadsheets showing adequate income and low unemployment completely fail to capture or predict.

This article is for informational purposes only and should not be construed as financial advice. Consult a financial professional before making investment or other financial decisions. The author and publisher make no warranties of any kind.